Money stands behind every project activity. It defines both the quality of your work and its outcomes. Yet since the majority of us don’t have unlimited resources to pour into our projects mindlessly, we need to carefully plan out the usage of the money at our disposal.

Project cost breakdown comes in handy in this regard, especially for growing businesses.

According to Robert Sher from Harvard Business Review:

“As companies grow from small to midsize, they inevitably arrive at a point where systematic cost analysis – a regular, automated process of evaluating all costs – is critical to their survival and continued growth.”

Let’s find out how to craft a project cost breakdown so it can help you with that (and how to automate cost tracking and analysis for better results).

Also, don’t forget to download our free cost breakdown structure (CBS) templates – they will simplify the planning and analysis processes + save you looots of time.

What Is Project Cost Breakdown?

Project cost breakdown (aka CBS) is a visual representation of all cost categories within a particular project. These usually include work and material costs, less often – outsourcing, logistics and overhead costs and rush fees – listed across every project activity.

Project cost breakdown can be used for the following purposes:

#1: Estimating the overall cost of work, analyzing the financial viability of a project, etc.

#2: Getting stakeholder approvals and support, coordinating project costs with clients.

In either case, your CBS must be clearly and logically structured. Of course, doing so is a tedious task but, in the end, it is bound to enhance your communication with clients and allow for a better understanding of how costs can be managed in the course of the project.

Main Components of a Cost Breakdown Structure

Here are the base components of a project cost structure:

#1: Key cost drivers: Expense items, work packages, specific tasks or services that incur costs, etc.

#2: Quantity: The number of items or materials, the amount of work time.

#3: Overhead or hidden costs: Costs that don’t bring any direct value but influence project work processes indirectly.

Depending on the purposes of your project cost breakdown and the project’s nature, you can group the cost data by different parameters:

By time periods

This data grouping can be used to estimate monthly, weekly, quarterly, or other costs. Usually, it is combined with grouping by workflow steps or milestones (e.g., project planning, design, final review, etc.) and includes a total for the entire project.

By cost types

When no time breakdown is required, structuring your data by cost types is a common approach.

It helps identify key cost drivers and their influence on the final project cost. Also, this approach is preferred when your CBS purpose is to define where some aspects of your project and manageable in terms of money and find out ways to decrease the total cost.

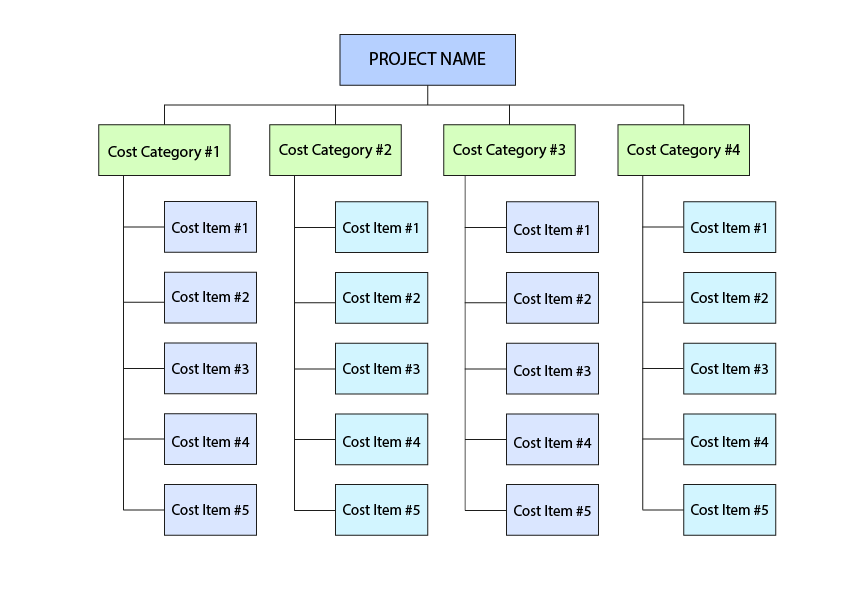

Project Cost Breakdown Example

Below is an example of what a CBS diagram looks like in its simplest form. Such a diagram can be crafted for each separate project phase. Plus, you can add more details to the picture by dividing cost items or cost categories into sub-groups if appropriate.

What Costs to Include in a Cost Breakdown Structure?

The final project cost is frequently divided into the following cost categories:

Labor costs also called direct costs, are the costs of employees’ time spent on rendering services or performing manufacturing works within the project. They can incur as work time paid at a specific pay rate or as a fixed cost per item, unit, or service.

Subcontracting / outsourcing costs are sometimes treated as direct costs, and sometimes included in cost structures as a separate category. Again, they can be accrued on the basis of work time spent by an outsourcing team and their pay rates, or as a fixed cost for certain products or services.

Material costs arise as costs of raw materials, parts, and supplies purchased for using in project works or performing them. Sometimes, this cost type also includes insurance, custom clearance and other costs related to purchasing materials and goods.

Logistics costs are associated with storing and moving purchased materials and include such subcomponents as transportation, storage, distribution, etc.

Overhead costs cannot be always allocated to a specific cost driver and don’t create profit in a direct way. However, they influence project outcomes indirectly by making business activities possible, or increasing their efficiency.

Common Mistakes in Structuring Project Costs

Humans make mistakes. Thus, if you’re creating a project cost breakdown manually, you must be extra careful to make sure your CBS is accurate. And let’s not forget about the risks that can affect your performance in the course of the project, as well as high unexpected costs.

Here are several common mistakes to be aware of and avoid in order to get better CBS results:

-

Omitting some cost drivers.

While carefully analyzing components of the final price is an essential part of the cost estimation process, some of the cost drivers can get omitted – this usually happens to the costs that can be allocated to different categories, or overhead costs.

-

Not including routine works like communications, organizational, and administrative works into the final cost estimate.

These works are hard to estimate and are rarely considered a direct cost driver, but this doesn’t mean they should not be included in the cost structure. A reasonable way to handle them is to include a rough estimate with a comment that the final cost will depend on time actually spent on these works.

-

Not including non-billable works if you’re using cost breakdown for internal reference.

The proportion between billable and non-billable works defines profitability of a project, so if you’re using cost breakdown for profitability analysis, make sure to take all types of project-related non-billable works into account.

Project Cost Breakdown by Pricing Type

The type of work pricing depends on the nature of projects, common practices in particular fields and industries, and the market environment. With any pricing type, accurate project cost breakdown is vital for project outcome and customer satisfaction.

Let’s take a look at the examples of how it can be used with different pricing types:

Cost per service or material

An accurate cost breakdown – both estimated or final – helps to coordinate project prices with customers as it explains what tasks you intend to complete and what exactly they will pay for.

However, in case clients agree on the final budget based on your CBS, sticking to it becomes critical – exceeding the stated costs will harm your reputation and damage trust with clients.

Cost per package

When this pricing method is used, customers pay a fixed price for a specific set of works, services, and/or products. That’s why, it is key to provide them with a clear picture of billable works for each package offered to them, and cost breakdown seems to be the most efficient way to show where billable time goes.

Cost breakdown structures for each package can also be used internally for analysis and adjustment of current package pricing.

Fixed price

Initially, customers know the final cost only, so you might need to prepare a cost breakdown for them. Customers tend to worry that they’re paying too high a price, and exact cost breakdown data helps justify specific cost of the project.

What’s more, cost breakdown can be used for internal analysis of project profitability. In this case, it should be centered around pay rates, business costs, operational/administrative costs, and include all non-billable works.

Make a Legit Project CBS in 5 Simple Steps

Step 1: Start with a Work Breakdown Structure (WBS)

A WBS is a hierarchical diagram outlining every major milestone and tiny piece of work you intend to complete during a project.

It breaks down the entire work scope bit by bit, starting from the overall project goals and ending with tiny work packages made of tasks. It delineates the relationships between each part of the project, which greatly assists in further work scheduling and estimation.

Find out more about the art of building a proper WBS in this guide and get a free WBS template here.

Step 2: Use our free project cost breakdown templates

Our free CBS templates provide a solid foundation to build your project cost breakdown on. We’ve included several template formats you can choose from depending on how detailed you want your CBS to be and how you want it to look:

- The Excel cost breakdown structure template allows you to record your versatile cost items thoroughly in the familiar table format. It divides a project by months. However, you can use milestones instead of periods if necessary. More importantly, it sums up expenses automatically, so there’s smaller risk of errors.

- The Word CBS template is similar to the Excel one (but without automation). However, it is easier to write additional information and comments in this textual format. So, use it when that extra level of detail is necessary.

- The PDF template has the form of a simple CBS diagram. Please note that you can edit it only if you are subscribed to Adobe Acrobat Pro or similar software.

- The JPEG CBS diagram is convenient to work with in printed form or in any digital editor of choice. Just fill out the empty slots with your project cost data and use it as a guideline during the work on your small projects.

- The Ai cost breakdown diagram is perfect for creatives who regularly work with Adobe Illustrator – editing it in your favorite tool is as easy as pie.

Fill out the below form to grab this essential cost breakdown templates pack for free!

Step 3: Estimate costs for each project task

Here are some of the best project estimation techniques you can use to predict how many expenses each work package or task is likely to incur:

Expert judgment

Experts’ opinions used to make up for the lack of clarity in existing cost breakdown can influence cost drivers where more predictability is required.

While this method is used to come up with more accurate estimates, a significant difference between the planned and the final figure is still possible because experts are people, and people make mistakes no matter how experienced or knowledgeable they may be.

To err is human, as they say. So, unless you get expert opinion from a supernatural entity, make sure to leave room for some uncertainty.

Analogous estimation

Comparing estimates based on cost breakdown for previous projects with new similar ones helps improve estimation results and get more accurate assessment of project costs, profitability, and general outcome.

However, we rarely can find two absolutely identical projects – each new one requires a slightly different approach and know-how. Thus, you can get 100% accurate results via analogous estimation only if your projects repeat themselves in every little aspect, and no unexpected external factor can suddenly influence your performance.

Otherwise, this estimation technique implies some degree of inaccuracy, which you can address by implementing additional forecasting and data analysis methods.

actiTIME features a multitue of project reports that provide invaluable historical data for analogous project estimation. You can analyze project costs, the use of time per task, and billable hours and compare them to your initial estimates to identify if anything went wrong.

Bottom-up analysis

Planned project costs are structured on the basis of the costs of small tasks, services, and product parts. High accuracy is achieved by taking into account all cost drivers, including costs of routine works, overhead, and possible additional costs.

As great as bottom-up analysis is, it doesn’t really work for large projects with myriads of cost items and resources involved. Estimating every little thing comprised in a project like that at once would become an everlasting nightmare.

A possible workaround to this problem is to apply bottom-up estimation to smaller segments or phases of large projects – such a task is significantly more manageable.

Top-down analysis

A top-down cost structure can be used for coming up with a ballpark estimate of the final figure. When using it, it’s essential to factor in various additional costs not included in the initial estimate.

Since this estimation technique aims at defining the pig picture, it actually works perfectly well for large projects (at least at the initial phases of work planning).

You start at the top with the overall project estimate and then slowly move down dividing that estimate by key project milestones or phases. Once done, you can proceed to breakdown those milestones into even smaller work packages or tasks. And finally, double-check how those tiny estimates fit within the overall picture.

Parametric estimation

According to PMI, “parametric estimating uses a statistical relationship between historical data and other variables (e.g., square footage in construction) to calculate an estimate for activity parameters, such as cost, budget, and duration. This technique can produce higher levels of accuracy depending upon the sophistication and underlying data built into the model.”

The accuracy comes at a price though – you need to understand how statistical analysis works and apply it correctly. Luckily, we now have a plethora of software tools available that can streamline even the most complex analysis processes. Yet be ready to spend a portion of your project budget on subscription (which is not always cheap, to say the least).

Step 4: Measure cost opportunities to choose the best action plan

A project breakdown structure can be used as a handy tool for financial planning.

Let’s say you’re planning out a marketing campaign and can’t decide on the final outreach methods: Should you collaborate with a SoMe influencer or invest in outdoor advertising?

A project cost breakdown structure will help you see how viable each of the desired methods will be and how they fit within your overall financial limits.

If a collaboration with the influencer turns out to be too expensive, you may think of some cheaper yet similarly effective methods to reach your target audience – that’s a good way to promote cost efficiency.

Step 5: Define your contingency margin

A contingency margin is a financial safety cushion that will protect your project from cost overruns in case something unexpected happens.

It’s vital to take all kinds of costs into account: direct, indirect, and overhead expenses. Then, allocate a reasonable buffer amount to each of these cost categories.

In case you need some help figuring out how much extra money to allocate here exactly, feel free to use our free risk assessment templates to identify everything that could go wrong and measure how those risks could impact your project performance and spending.

Grab them here.

The Role of Project Cost Breakdown in Budgeting

A CBS is an essential budgeting tool.

First of all, it requires you to make a thorough plan of project tasks and activities you need to complete. On top of that, it lists all cost estimates in detail. That’s why it simplifies the budgeting process a great deal:

You don’t have to craft a budget from scratch! Just use the estimates from your project cost breakdown, sum them up, and you get to how much money overall you need to invest in your project. Just double-check everything, fine-tune the figures with the bigger strategic picture, and you’re all set.

Want to simplify the budgeting process even more?

Download our free project budget tracking templates here or sign up for actiTIME trial to leap from zero to hero at once!

As a multifunctional project management tool, actiTIME has it all to help you streamline budget management and track project costs with ease:

- Start by planning out your entire project scope: create tasks, set deadlines and priorities, and assign work to your team members.

- Set bespoke pay rates for employees to track staff-related project expenses by hour of regular work, time off, and overtime.

- Set billing rates for different types of work to monitor your hourly revenues as well.

- Allocate cost, billing, and time budgets at three different levels: entire projects and customers, or each individual task.

- Track the use of resources ongoingly via a visual progress bar – it colors project overruns in red to help you detect and address them promptly.

- Use diverse reports to analyze your cost tracking data in depth, compare actual results to initial estimates, and see how profitable your work is.

actiTIME makes it easy to track all your project resources in a single place. Check the above (and many other) features in action to see how they can simplify your cost management process and promote superior financial outcomes.

Project Breakdown Structure FAQs

What is cost breakdown analysis?

This type of analysis allows you to comprehend how the various cost items from your CBS contribute to the overall price of a product, service, or project you work on.

It requires you to dissect and examine each cost category and item in order to find any areas of inefficiency, pinpoint cost drivers, and make evidence-based decisions to optimize your operations.

By means of cost breakdown analysis, you can learn how to reduce costs, implement profitable pricing strategies, and drive the overall financial success of your business.

Cost Breakdown Structure vs. Work Breakdown Structure

While the CBS is all about project expenses, the WBS is primarily concerned with project deliverables. In other words, it’s focused on team performance rather than financial performance or budget allocation.

By outlining your work plan in considerable detail, it serves as a great basis for building your CBS – pretty much, you just need to assign cost estimates to every work package and then sum them up at higher levels.

Cost Breakdown Structure vs. Resource Breakdown Structure

The Resource Breakdown Structure (RBS) is a detailed outline of project resources, categorized by type and function. Although it can contain the info on resource estimates, they are not a central part of the document.

Just like a WBS, an RBS provides a solid foundation for crafting a project cost breakdown – resources cost money, so listing every single item you need to complete your tasks will help you estimate expenses well.

Why is project cost breakdown important?

We all understand what a proper project cost breakdown is needed for – at the base level, it helps to manage cost-related risks better and provides a good foundation for project budgeting.

Yet did you know that it also serves to protect your reputation as a project manager?

Your goal is to ensure that your project is delivered on time and no unexpected expenses take place while delivering it. Of course, you can take a risk and proceed to work without making a CBS beforehand. However, in that case, a cost overrun is more likely to occur, and the bigger it gets, the more serious damage to your reputation comes along.

A carefully crafted project cost breakdown will help you avoid that.

Ready to enhance your project cost management, secure your professional reputation, and track expenses more accurately? Start using actiTIME today.

![13 Best On-Premises Business Software Tools [2026]](https://www.actitime.com/wp-content/uploads/2020/05/self-hosted-business-products.png)